Agentic AI refers to advanced artificial intelligence systems that operate autonomously to achieve complex goals with minimal human intervention. These systems use reasoning, planning, memory, and external tools to perceive environments, make decisions, and adapt actions dynamically.

Core Features

Agentic AI excels in goal-oriented behavior, breaking down multi-step tasks through iterative planning and execution. It leverages large language models (LLMs) as a “brain” for natural language understanding and integrates with tools like APIs for real-world actions. Unlike generative AI, which focuses on content creation, agentic AI emphasizes proactive orchestration across systems.

Key Differences

Applications

In enterprise settings, agentic AI handles workflows like customer service personalization or software development by analyzing data and coordinating actions. It suits dynamic fields such as auditing or cybersecurity, where it could predict risks or automate compliance checks autonomously.

Applications of Agentic AI in Financial Auditing:

Agentic AI, which involves autonomous systems capable of perceiving, reasoning, and acting independently, is transforming financial auditing by automating complex, multi-step tasks like data analysis and risk assessment.

Key Applications

Journal entry testing: Agents iteratively query systems, validate entries, and generate reports, as shown in frameworks shifting from co-piloted to auto-piloted auditing.

Continuous monitoring and anomaly detection: Real-time scanning of datasets for risks, fraud, and compliance issues, reducing manual efforts in internal audits.

Data reconciliation and fraud surveillance: Autonomous matching across systems, pattern learning, and proactive alerts, accelerating closes and improving accuracy.

2. RESEARCH QUESTION

To what extent do multi-agent systems in agentic AI, as implemented in Big Four platforms like Deloitte Omnia and KPMG Clara, EY.ai and PwS Agent OS enable continuous auditing and full-dataset risk management in financial auditing while addressing regulatory compliance and hallucination risks by 2030?

3. TARGETED AUDIENCE

Audit Practitioners and Firms (especially the Big Four): Provides a roadmap for adopting Agentic AI, benchmarks for efficiency gains, and insights into transitioning to continuous, full-dataset auditing.

Regulators and Standard-Setting Bodies (e.g., ICAI, PCAOB, COSO): Highlights the need for updated governance frameworks, AI evidence admissibility standards, and safeguards against risks like hallucinations and cyber vulnerabilities.

Technologists and AI Developers: Outlines technical requirements (e.g., multi-agent orchestration, explainable AI) and validation strategies to build robust, trustworthy audit systems.

Academia and Researchers: Serves as a foundation for future empirical studies and cross-jurisdictional research on autonomous auditing.

4. OBJECTIVES OF THE STUDY

Comparative Analysis of Agentic AI in Big Four Audit Platforms (2025–2026 → 2030 Projection)

To examine key technologies like multi-agent orchestration, continuous auditing, and quantum AI integration, while addressing explainability and auditability requirements.

To identify challenges (e.g., legacy system scalability, cybersecurity risks, regulatory gaps) and propose solutions, including governance frameworks, hallucination safeguards, and policy alignment with COSO (Committee of Sponsoring Organizations of the Treadway Commission) / PCAOB (Public Company Accounting Oversights Board) standards.

To advocate for accelerated adoption of Agentic AI as the cornerstone of future financial auditing through collaborative innovation among firms, regulators, and technologists.

5. RESEARCH METHODOLOGY AND DATA COLLECTION METHODS

In this research study, conceptual and case study analysis research strategies are used. For this purpose, secondary data have been collected from various sources such as the official e-domains of Big Four implementations – Deloitte Omnia, KPMG Clara, EY.ai and PwC Agent OS, e-books, and e-magazines.

6. REVIEW OF LITERATURE

The evolution of Artificial Intelligence (AI) in financial auditing reflects a paradigm shift from assistive analytics toward autonomous, agent-driven ecosystems. Recent literature indicates that Agentic AI—defined as multi-agent systems capable of planning, reasoning, and autonomous execution—is emerging as a transformative force in audit assurance frameworks. Early AI adoption in auditing focused on machine learning (ML)–based anomaly detection and cognitive analytics. Brown-Liburd, Helen and Vasarhelyi, Miklos (2020) highlighted how AI enhances fraud detection accuracy and enables full-population transaction testing, reducing reliance on statistical sampling. However, their findings emphasized the necessity of structured governance mechanisms to maintain auditor accountability in AI-supported environments. These insights provide the conceptual foundation for the transition toward autonomous audit agents.

Subsequent research by Issa, Hussein, Sun, Ting, and Vasarhelyi, Miklos (2021) demonstrated that deep neural networks outperform classical regression-based audit models in anomaly detection tasks. While detection accuracy improved significantly, the authors identified critical limitations in interpretability and audit-trail transparency. These limitations directly influence the design of future Agentic AI systems, which must incorporate explainability-by-design architectures such as chain-of-thought logging and traceable reasoning paths.

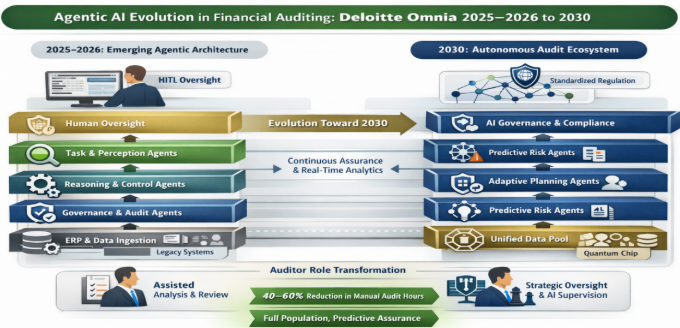

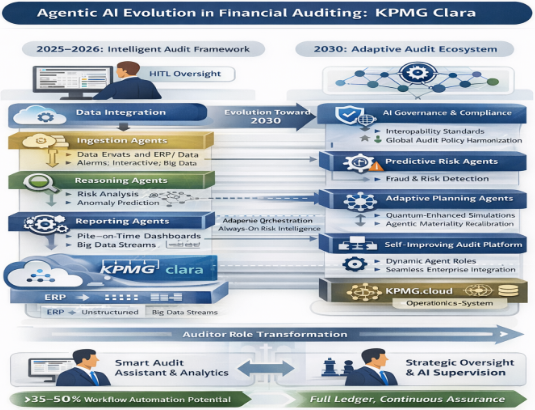

The intermediate phase of Robotic Process Automation (RPA) marked the operational shift toward automation. Kokina, Julia and Blanchette, Sherrie (2022) reported efficiency gains of up to 50% in repetitive audit procedures through RPA deployment. However, RPA systems lack adaptive intelligence and contextual reasoning, reinforcing the need for next-generation agentic architectures capable of dynamic decision-making. From 2023 onward, large-scale industry implementations signal the emergence of Agentic AI ecosystems. The Deloitte Omnia platform demonstrates continuous auditing capabilities using predictive analytics and ML pipelines for real-time transaction monitoring. Similarly, KPMG Clara integrates cloud-based NLP tools and collaborative analytics to enhance regulatory compliance. These systems represent foundational steps toward autonomous audit agents but remain partially human-supervised.

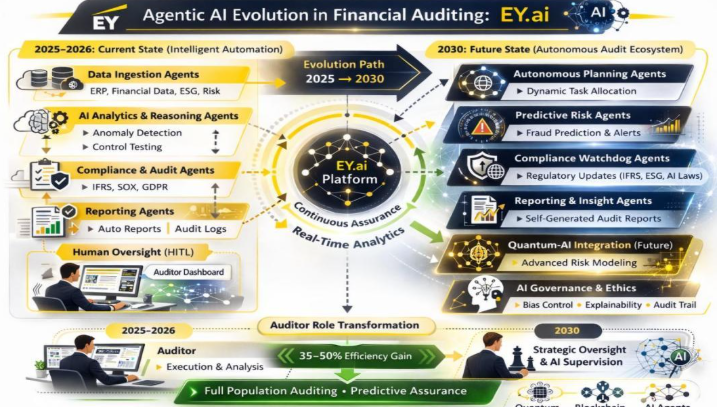

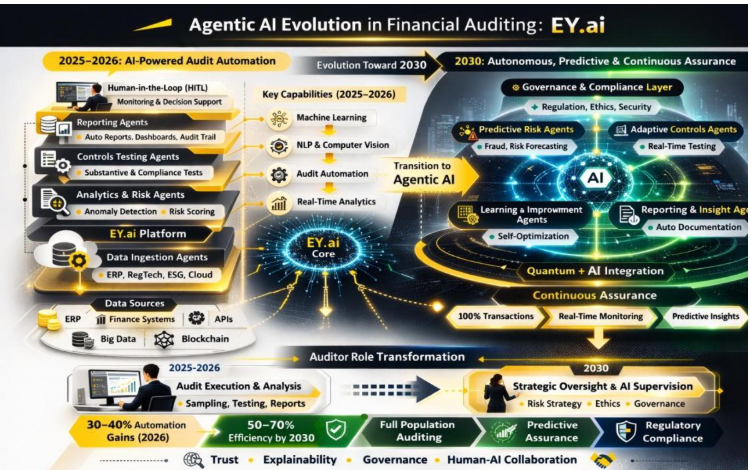

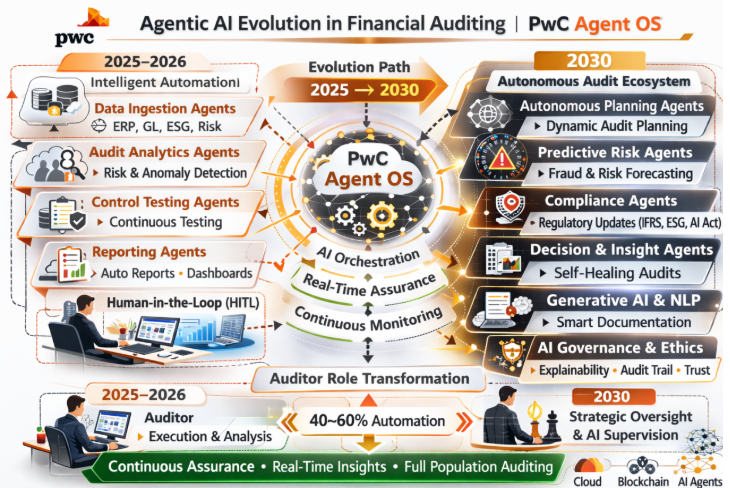

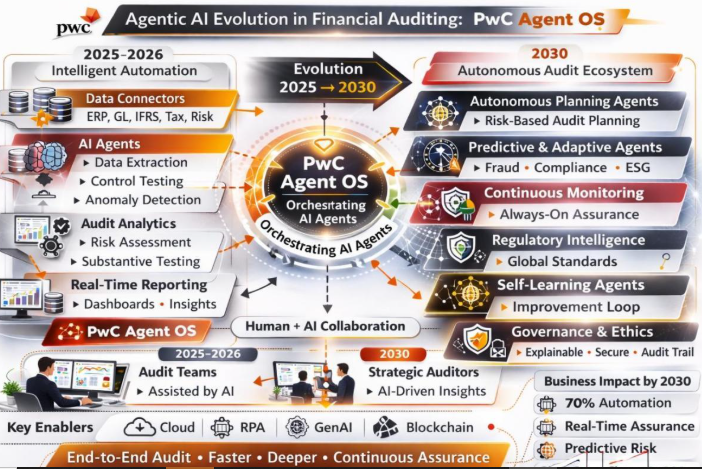

More advanced orchestration models are observed in EY AI initiatives and PwC Agent OS frameworks, where multi-agent configurations coordinate ingestion, control testing, reasoning, and reporting tasks. Such systems employ generative AI, reinforcement learning, and Retrieval-Augmented Generation (RAG) to enable adaptive compliance with evolving standards such as IFRS and GDPR. These developments indicate that future audit platforms will shift toward continuous, real-time assurance supported by autonomous planning agents.

Despite rapid advancement, significant research gaps remain. First, standardized benchmarking frameworks for agent robustness and reliability are underdeveloped. Second, empirical cross-jurisdictional studies validating AI-generated audit evidence under PCAOB and international regulatory regimes are limited. Third, cybersecurity vulnerabilities—such as prompt injection and adversarial manipulation—pose emerging risks in agent-based audit environments. Finally, ethical AI governance and bias quantification models require further formalization to ensure trustworthiness.

In summary, the literature indicates that the future of financial auditing lies in fully orchestrated Agentic AI ecosystems characterized by continuous monitoring, explainable reasoning, adaptive compliance, and hybrid human–AI collaboration. However, achieving scalable, secure, and regulatorily admissible autonomy remains the central challenge for future research in Agentic AI for financial auditing.

7. BIG FOUR IMPLEMENTATION

Comparative Analysis of Agentic AI in Big Four Audit Platforms (2025–2026 → 2030 Projection)